From market access to margins, carbon now influences every major business metric — and delay comes with real financial risk.

Introduction

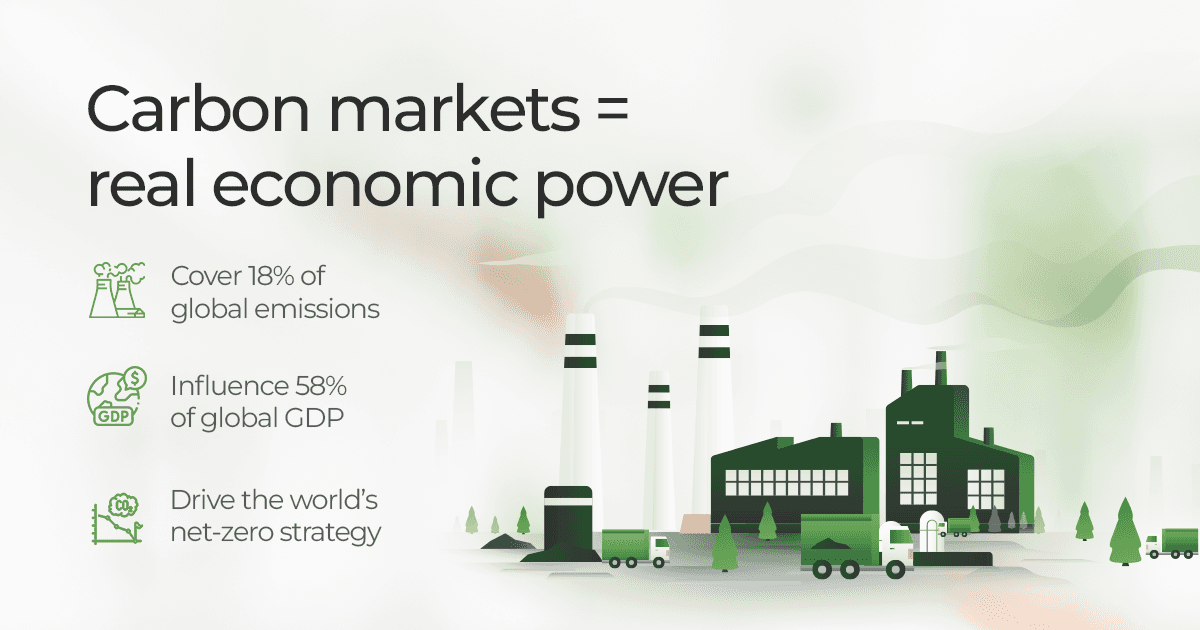

The net-zero transition is no longer a distant ambition - it is a present economic reality. More than 90% of global GDP is now covered by net-zero commitments (UNFCCC), and carbon policies are rapidly reshaping how countries trade, invest, and regulate industries. Carbon markets, once considered fringe mechanisms, now influence 58% of global GDP and continue to expand through instruments like the EU’s Carbon Border Adjustment Mechanism (CBAM) and emerging emissions trading systems across Asia and Africa.

For Indian manufacturers, heavily integrated into global supply chains, this shift is both exposure and opportunity. As buyers demand verified emissions data and low-carbon products, carbon is becoming a cost of doing business, not just a sustainability metric. Manufacturers who treat carbon as a new economic system, one with real prices, risks, and financial upside will be better positioned to compete, access capital, and lead in global value chains.

The Rise of the Global Carbon Economy

Carbon is no longer just an environmental issue — it has become one of the world’s most important economic variables. Today, 23 carbon pricing instruments are operational globally, covering nearly 18% of all global emissions (World Bank State of Carbon Pricing 2024). With the EU ETS alone trading over €870 billion in carbon allowances in 2023, carbon has become one of the fastest-growing asset classes in global finance.

This shift is not limited to Europe. China operates the world’s largest emissions trading system, while emerging markets including South Korea, Indonesia, Kazakhstan, and several African economies are rapidly moving toward carbon pricing. As more countries deploy ETS mechanisms or border carbon taxes, carbon becomes embedded into the cost structure of traded goods.

For Indian manufacturers, this means the global carbon economy is not optional, it is unavoidable. More than 70% of India’s merchandise exports go to regions that have active or upcoming carbon pricing policies, making carbon a critical determinant of trade competitiveness.

Companies that build carbon readiness now will have a structural advantage, lower financial exposure, stronger export resilience, and early access to climate-linked capital and incentives. The carbon economy is no longer emerging. It has already arrived.

Why Indian Manufacturers are in the Direct Line of Fire

Indian manufacturers are facing unprecedented exposure to the global carbon economy not because of domestic policy alone, but because their largest customers and export destinations are enforcing carbon accountability across entire supply chains.

1. The EU CBAM has changed the rules of global trade

The EU Carbon Border Adjustment Mechanism (CBAM) is now in force, requiring exporters of steel, aluminium, cement, chemicals, and electricity to report embedded emissions and soon, to pay for them.

By 2030, CBAM could impose costs equivalent to 20–35% of product value for carbon-intensive exporters (EU Commission Impact Assessment). India is one of the top five countries exposed to CBAM.

2. Global OEMs are pushing Scope 3 reduction upstream

Over 65% of Fortune 500 companies now have net-zero or science-based targets, which include emissions from suppliers (Scope 3). This means automotive, electronics, FMCG, aerospace, and retail giants are demanding:

Verified emissions data

Decarbonisation roadmaps

Low-carbon materials

Lifecycle transparency

Indian Tier 1 and Tier 2 suppliers are under rising pressure to align — or risk being replaced.

3. Capital markets are penalising high-carbon businesses

Global financial institutions representing $150 trillion AUM have committed to net-zero financing (GFANZ).

High-carbon sectors now face:

Higher cost of capital

Tighter lending criteria

Reduced access to global investment pools

Meanwhile, green manufacturing and clean-tech projects receive premium financing terms.

4. India’s own policies are tightening

India is introducing carbon markets, mandatory sustainability reporting (BRSR Core), and clean energy obligations. This means domestic manufacturers will face compliance even if they don’t export.

In short: Indian manufacturers are not just participants in the carbon economy, they are becoming one of its most heavily impacted groups.

The Financial Risks of Ignoring Carbon

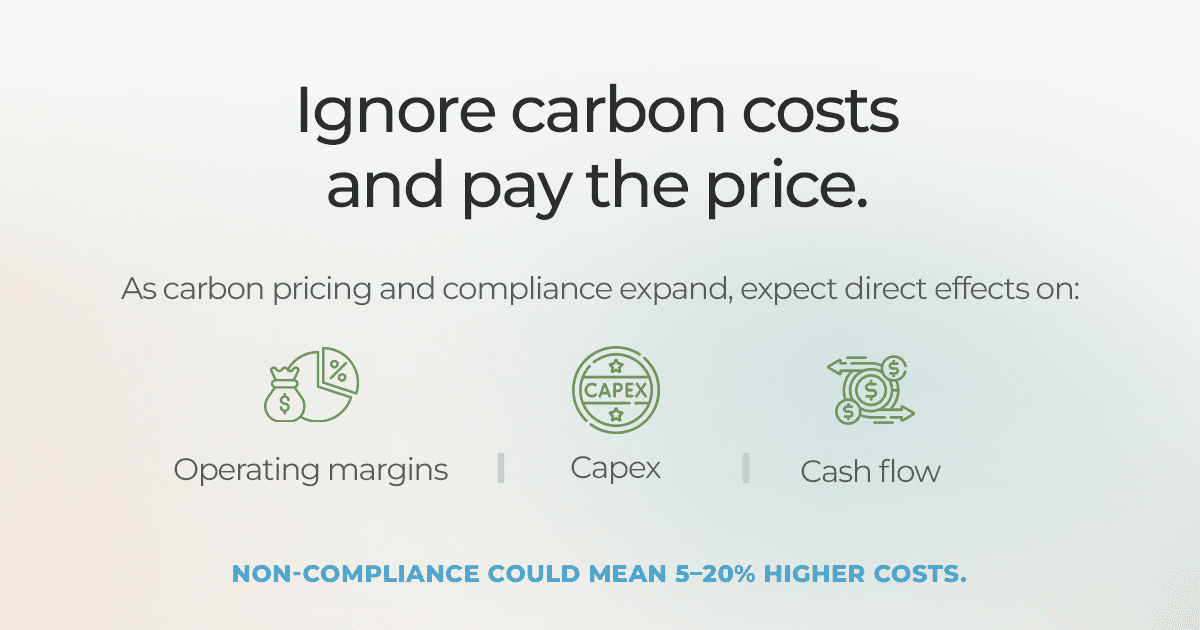

For Indian manufacturers, carbon is no longer an abstract sustainability metric — it is a direct financial variable that influences margins, competitiveness, and long-term viability. Companies that fail to prepare will face rising and compounding costs across multiple fronts.

1. Carbon pricing = higher operating costs

As global and domestic carbon pricing instruments expand, high-emission manufacturers will face immediate cost increases.

A 2024 IEA analysis shows that carbon prices globally are rising at 12–18% CAGR, and could reach $100–$150 per tonne by 2030 for traded sectors (IEA Tracking Clean Energy Progress).

For Indian exporters, this could translate into:

5–20% increase in cost of goods

Reduced margins on long-term contracts

Pressure from OEMs to absorb the carbon cost instead of passing it on

2. New compliance regimes will hit cash flow

Mechanisms like CBAM, BRSR Core, and global supply-chain audits require:

Product-level emissions data

Supplier-level disclosures

Lifecycle assessments

Evidence-backed reporting

Companies unprepared for this will incur sudden, high compliance spend often 3× higher when done reactively instead of proactively (McKinsey Sustainability Benchmark 2023).

3. Loss of market access

Non-compliance or lack of carbon transparency is already resulting in:

Disqualification from global procurement

Reduced export volumes

Loss of preferred supplier status

A WEF survey found that 57% of global buyers are actively switching suppliers based on sustainability performance.

4. Capital becomes more expensive

Banks and investors increasingly penalise high-carbon companies with:

Higher interest rates

Lower credit limits

Restrictive lending terms

Meanwhile, the IFC estimates that emerging markets lose $50–$100 million annually per sector in financing opportunities due to poor climate disclosures.

Ignoring carbon is no longer a passive choice, it is a direct financial risk that compounds every year.

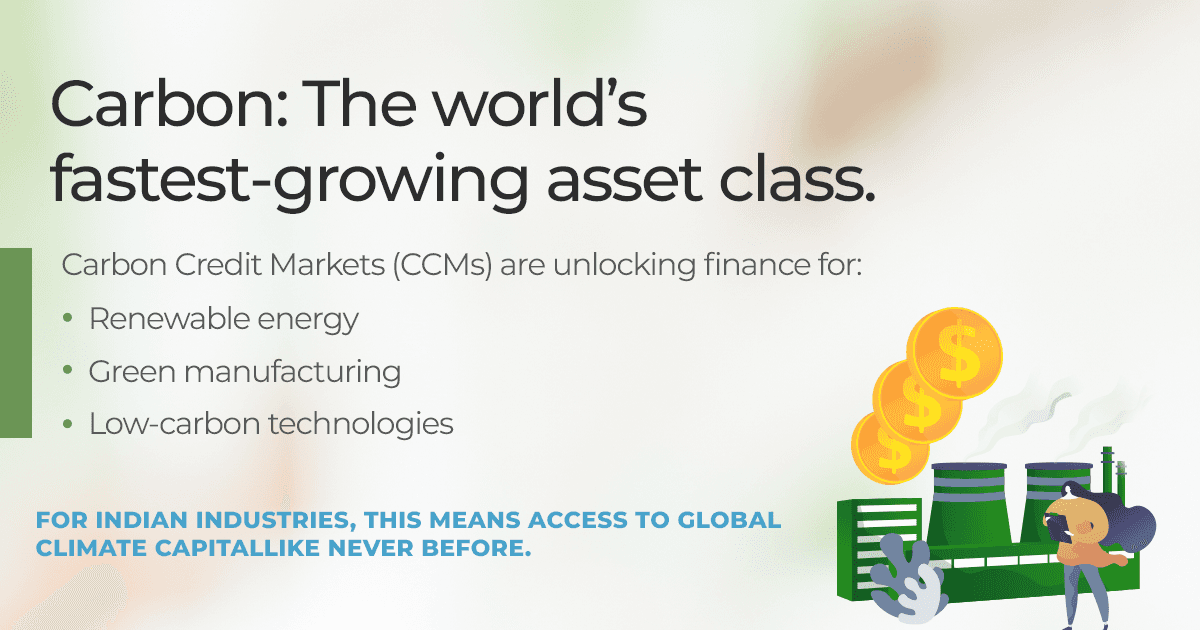

The Opportunity — Why Carbon Markets can become a Growth Engine for Indian Manufacturing

While carbon pricing increases pressure, carbon markets also unlock enormous upside for Indian manufacturers. Instead of treating carbon as a compliance cost, leading companies are now recognising it as a new economic system — one that rewards efficiency, innovation, and low-carbon production.

1. Carbon markets are unlocking unprecedented climate finance

The global voluntary carbon market (VCM) is expected to grow 5–10× by 2030, reaching $30–50 billion (McKinsey VCM Outlook). Compliance carbon markets like the EU ETS already exceed $870 billion in annual trading volume.

For Indian companies, this means:

New revenue streams from generating carbon credits

Access to global climate-linked capital

Funding for energy efficiency and low-carbon technology upgrades

India has one of the world’s largest renewable energy bases, making it uniquely positioned to benefit from credit generation once the Indian Carbon Market (ICM) becomes fully operational.

2. Low-carbon products command premium pricing

Global buyers increasingly prefer materials with lower embodied carbon. A Deloitte survey found that sustainable products gain 5–10% higher price premiums, especially in sectors like automotive, textiles, FMCG, and metals.

This provides Indian manufacturers a clear competitive edge if they can demonstrate:

Lower emissions intensity

Higher recycled content

Verified lifecycle data

3. Participation in carbon markets builds export resilience

Companies that track and reduce carbon can retain and even grow, their share in CBAM markets, where transparency gives suppliers a major advantage.

4. Carbon readiness strengthens long-term valuation

Firms with strong ESG performance have:

10–20% higher valuation multiples (MSCI)

More stable cash flows

Easier access to international debt and equity markets

What Indian Manufacturers Need To Do now — A Practical Roadmap

The carbon economy is evolving fast. Winning in this landscape requires structured, phased action — not scattered sustainability attempts. Indian manufacturers can follow a clear four-step roadmap to stay compliant, competitive, and investment-ready.

Step 1: Get Your Carbon Inventory Right (Scope 1, 2 & 3)

Most companies underestimate their emissions simply because they lack reliable data. Before any reduction strategy or carbon market participation, manufacturers must:

Create a digital, auditable emissions baseline

Map hotspots across energy, process fuel, materials, logistics, and waste

Bring supply-chain (Scope 3) contributors into the data loop

Platforms like Onlygood automate data capture, reconcile inconsistencies, and generate audit-ready inventories — a critical first step.

Step 2: Assess Regulatory Exposure & Financial Risk

Identify which upcoming policies impact you:

Indian Carbon Market (ICM)

EU CBAM

BRSR Core

Sectoral energy efficiency mandates

OEM decarbonisation targets

Run scenario models to understand how carbon prices — ₹1,000, ₹3,000, or ₹6,000/tCO₂e — affect margins, capex, and cash flow. This determines where action is most urgent.

Step 3: Build a Reduction Pathway That Aligns with Business Goals

This includes:

Energy efficiency upgrades

Renewable energy adoption

Process optimisation

Material substitution

Waste heat recovery

Supplier decarbonisation initiatives

Set short-term (12–18 month) and long-term (2030–2040) targets backed by ROI analysis.

Step 4: Monetise, Don’t Just Comply

Once emissions baselines and reduction plans are in place, companies can:

Generate carbon credits

Trade within the upcoming Indian Carbon Market

Access concessional finance and green funds

Secure preferential treatment from global OEMs

Carbon markets reward early movers; delay erodes competitive advantage.

The Strategic Advantage — Why Carbon Readiness is a Competitive Necessity for India

For Indian manufacturers, carbon readiness is no longer a sustainability choice, it is a strategic, commercial, and geopolitical necessity. As global supply chains decarbonise, India stands at a rare inflection point: positioned to become the world’s preferred low-carbon manufacturing hub or to lose ground to more prepared economies.

Carbon-efficient production is rapidly becoming a procurement requirement for sectors like automotive, electronics, heavy engineering, FMCG, and textiles. OEMs are rewriting supplier contracts to include Scope 3 expectations, lifecycle footprints, and annual carbon disclosures. Manufacturers that fail to adapt will see reduced order volumes, tougher audits, and ultimately replacement by competitors with cleaner processes.

At the same time, carbon-aligned industries gain a distinct cost and market edge. They attract lower-cost capital, win long-term global contracts, qualify for green subsidies, and access climate-linked financial instruments. Early movers benefit disproportionately because carbon-efficient systems compound over time.

For India, the opportunity is even bigger: with a young industrial base, strong renewable capacity, and expanding digital infrastructure, the country can build a global competitive moat by becoming a leader in low-carbon production.

In the carbon economy, competitiveness is not just price and performance, it’s carbon per unit of value. Manufacturers who optimise it will own the next decade.

Conclusion: The Cost of Waiting is Greater than the Cost of Acting

The carbon economy is no longer a distant policy concept, it is now shaping trade flows, investment decisions, supply chain structures, and competitive advantage. For Indian manufacturers, ignoring it is not just risky; it is existential. Carbon will influence every major business metric - margins, market access, procurement eligibility, compliance costs, and long-term enterprise value.

But the opportunity is equally powerful. Manufacturers who invest early in carbon measurement, reduction pathways, and market participation will outperform peers, attract global buyers, and tap into new revenue sources through climate finance, low-carbon products, and carbon credit markets.

The message is clear: Carbon readiness is the new currency of global manufacturing.

This is the moment for Indian industry to move from awareness to action to measure, integrate, and monetise carbon as a strategic asset. Those who prepare now will define the future of India’s industrial growth. Those who delay may not get a second chance.