Why Sustainability Reporting Feels Overwhelming Today

Over the past decade, ESG reporting has moved from a voluntary communications exercise to a regulatory, investor-driven, and supply-chain-mandated requirement. What was once a sustainability report published annually for reputational purposes is now a complex system of disclosures tied to capital access, procurement eligibility, and legal compliance.

Today, companies operate in a landscape of 600+ sustainability frameworks, standards, and rating systems globally. While not all are mandatory, many influence investment decisions, lender assessments, and customer procurement criteria. From global standards like GRI and ISSB to jurisdiction-specific regulations such as CSRD in the European Union and BRSR in India, reporting expectations are multiplying and converging at once.

At the same time, CSRD readiness is raising the bar. The regulation requires structured disclosures under the European Sustainability Reporting Standards (ESRS), introduces the principle of double materiality, and mandates assurance. This means organizations must evaluate not only how sustainability issues affect financial performance (financial materiality), but also how their operations impact the environment and society (impact materiality). The analytical depth and documentation required are significantly higher than traditional ESG disclosures.

Overlay this with Scope 3 reporting complexity, arguably the most demanding aspect of climate disclosure. Scope 3 emissions require companies to measure and manage emissions across their entire value chain, including suppliers, logistics, product use, and end-of-life treatment. This demands supplier engagement, data harmonization, estimation methodologies, and boundary decisions that go far beyond internal data collection.

Simultaneously, investor scrutiny has intensified. Asset managers increasingly align with ISSB and TCFD-style climate disclosures, demanding consistent governance, risk, and transition planning information. Rating platforms such as EcoVadis and CDP apply their own scoring methodologies, while national requirements like BRSR add another compliance layer for listed entities. Each system asks similar questions but in different formats, levels of detail, and timelines.

The cumulative effect on ESG teams is significant:

Duplicate data requests across frameworks

Manual, spreadsheet-based sustainability reporting

Rebuilding disclosures from scratch each cycle

Inconsistent numbers appearing across reports

Escalating audit and assurance risk

Growing internal compliance fatigue

From an organizational theory perspective, this reflects what scholars describe as institutional complexity when multiple regulatory, normative, and market forces impose overlapping but slightly divergent expectations on firms. Without integrated systems, organizations respond reactively, creating parallel reporting tracks rather than unified governance structures.

The critical insight is this:

The overwhelm is not fundamentally caused by the number of sustainability frameworks. It is caused by fragmented ESG data systems attempting to respond to each framework independently.

When sustainability data lives in disconnected spreadsheets, across departments, and without consistent governance, every new disclosure requirement feels like a new beginning. The result is compliance panic instead of strategic clarity.

The Hidden Common Ground Across Reporting Standards

At first glance, the global landscape of sustainability frameworks appears fragmented and even contradictory. GRI emphasizes impact materiality. SASB focuses on financially material industry metrics. TCFD centers on climate-related risk governance. ISSB consolidates investor-focused sustainability disclosure. CSRD introduces double materiality and mandatory assurance.

Different philosophies. Different audiences. Different structures.

Yet when examined at the data layer, these standards converge far more than they diverge.

The Architecture Beneath the Frameworks

Most major ESG reporting standards whether voluntary or regulatory are built around a shared structural architecture:

Governance

Strategy

Risk & Opportunity Management

Metrics & Targets

This structure is explicit in TCFD and ISSB, embedded within CSRD’s ESRS framework, reflected in SASB’s industry standards, and operationalized through GRI disclosures. Even scoring platforms like CDP and EcoVadis ultimately assess performance across these same domains.

The difference lies not in what is being measured but in how it is framed.

Governance: A Universal Expectation

Across frameworks, companies are asked to disclose:

Board oversight of ESG risks

Management accountability

Integration of sustainability into decision-making

Risk management processes

Whether under ISSB’s IFRS S1, TCFD’s governance pillar, CSRD’s ESRS 2, or GRI’s governance disclosures, the underlying expectation is identical: sustainability must be embedded in corporate governance structures.

Climate & Scope 1, 2, 3 Reporting

The convergence is even more visible in climate disclosure.

Nearly all major standards require:

Scope 1 emissions

Scope 2 emissions

Increasingly, Scope 3 reporting

Reduction targets

Transition plans

The methodology may reference different protocols or boundaries. The materiality lens may vary. But the underlying data energy consumption, fuel use, emission factors, supplier activity data remains the same.

In practice, one robust carbon accounting system can serve GRI 305, ISSB climate disclosures, CSRD ESRS E1, CDP submissions, and investor questionnaires simultaneously.

Materiality: Different Lenses, Shared Mechanics

CSRD formalizes double materiality.

ISSB prioritizes financial materiality.

GRI focuses on impact materiality.

But all require:

Structured materiality assessment processes

Stakeholder engagement

Documentation of risks and opportunities

Linkage to strategy and targets

The methodology and narrative emphasis differ the analytical process does not.

Social & Workforce Metrics

Across GRI, SASB, CSRD, and ISSB-related risk disclosures, companies repeatedly report on:

Workforce composition

Gender diversity

Health and safety performance

Training and development

Employee turnover

These metrics originate from the same HR and operational systems. The variation is in presentation and threshold, not in the underlying dataset.

Supply Chain & Due Diligence

Modern ESG reporting increasingly extends beyond direct operations. CSRD, ISSB climate disclosures, and rating platforms now emphasize:

Scope 3 supplier emissions

Human rights due diligence

Value chain transparency

Risk screening mechanisms

This expansion increases complexity but it does not introduce entirely new data categories. It requires deeper governance, verification, and traceability of information companies already partially collect.

The Core Insight

When sustainability reporting is viewed from the surface the report structure, the terminology, the regulatory context it appears fragmented.

When viewed from the data layer emissions data, governance structures, workforce metrics, risk registers the overlap becomes unmistakable.

The fragmentation exists at the reporting layer.

The convergence exists at the sustainability data layer.

Recognizing this distinction is critical. It shifts the conversation from “How do we comply with this new framework?” to “Do we have a governed ESG dataset capable of serving any framework?”

And that shift is where reporting begins to move from reactive compliance to structural readiness.

The Cost of a Reactive, One-Framework-at-a-Time Approach

If sustainability frameworks overlap so significantly at the data level, why does ESG reporting still feel so resource-intensive?

Because most organizations approach each new requirement as a standalone compliance project.

A new regulation emerges such as CSRD.

An investor demands ISSB-aligned disclosure.

A customer requests EcoVadis scoring.

A rating agency sends a CDP questionnaire.

And the cycle begins again.

The “Reset” Problem

In many companies, sustainability reporting operates in annual cycles rather than continuous systems. Each reporting period triggers:

Fresh data calls to departments

Manual consolidation in spreadsheets

Reinterpretation of definitions

Last-minute clarifications

Reconciliation of inconsistencies

This phenomenon resembles what management theory describes as path dependency where past ad hoc solutions shape future inefficiencies. Instead of building integrated systems, organizations layer temporary fixes on top of legacy processes.

Over time, this creates structural fragility.

The Hidden Costs of Compliance Fatigue

A one-framework-at-a-time approach generates visible and invisible costs:

1. Duplicate Data Collection: Teams repeatedly gather similar data for GRI, CSRD, CDP, and internal reporting often in slightly different formats.

2. Inconsistent Disclosures: Minor definitional differences in Scope 3 reporting or boundary assumptions can result in conflicting numbers across reports.

3. Spreadsheet Risk: Manual ESG reporting increases the likelihood of calculation errors, version control issues, and audit exposure.

4. Escalating Assurance Burden: As CSRD readiness requirements expand and third-party assurance becomes mandatory, weak documentation and fragmented systems create verification challenges.

5. Internal Trust Erosion: Finance, operations, procurement, and HR teams may begin to view sustainability as repetitive and disruptive rather than strategic.

Strategic Consequences Beyond Compliance

The most significant cost is not operational, it is strategic.

When ESG teams spend the majority of their time responding to disclosure requests, they have limited capacity to:

Improve decarbonisation pathways

Strengthen supplier engagement

Use sustainability scoring for benchmarking

Align ESG strategy with capital allocation

In effect, sustainability becomes an administrative burden rather than a driver of business resilience.

From an organizational design perspective, this is a classic case of reactive governance where systems evolve in response to external pressure rather than internal architecture. The result is compliance instability.

Why This Approach Cannot Scale

As sustainability regulation accelerates globally particularly with CSRD implementation and ISSB alignment the reporting burden will increase, not decrease. Scope 3 reporting requirements will deepen. Double materiality assessments will become more rigorous. Assurance standards will tighten.

A reactive model that rebuilds disclosures each year is not scalable in this environment.

The issue is not effort.

It is structured.

Without a centralized, governed ESG data system, every new sustainability framework will feel like a new reporting crisis.

And that is what keeps organizations trapped in compliance fatigue rather than advancing toward future-ready sustainability reporting.

Building a Core Sustainability Dataset That Works Everywhere

If the overwhelm is structural, then the solution must also be structural.

The shift from compliance fatigue to future-ready sustainability reporting begins with a simple but powerful idea:

Separate data architecture from reporting format.

Instead of building disclosures around frameworks, organizations must build a core sustainability dataset that can serve any framework whether GRI, ISSB, CSRD, SASB, CDP, BRSR, or future standards yet to emerge.

What Is a Core Sustainability Dataset?

A core sustainability dataset is a governed, continuously updated repository of material ESG parameters across environmental, social, and governance dimensions.

It is not a report.

It is not a questionnaire response.

It is not a one-time data collection exercise.

It is the structured foundation beneath all ESG reporting.

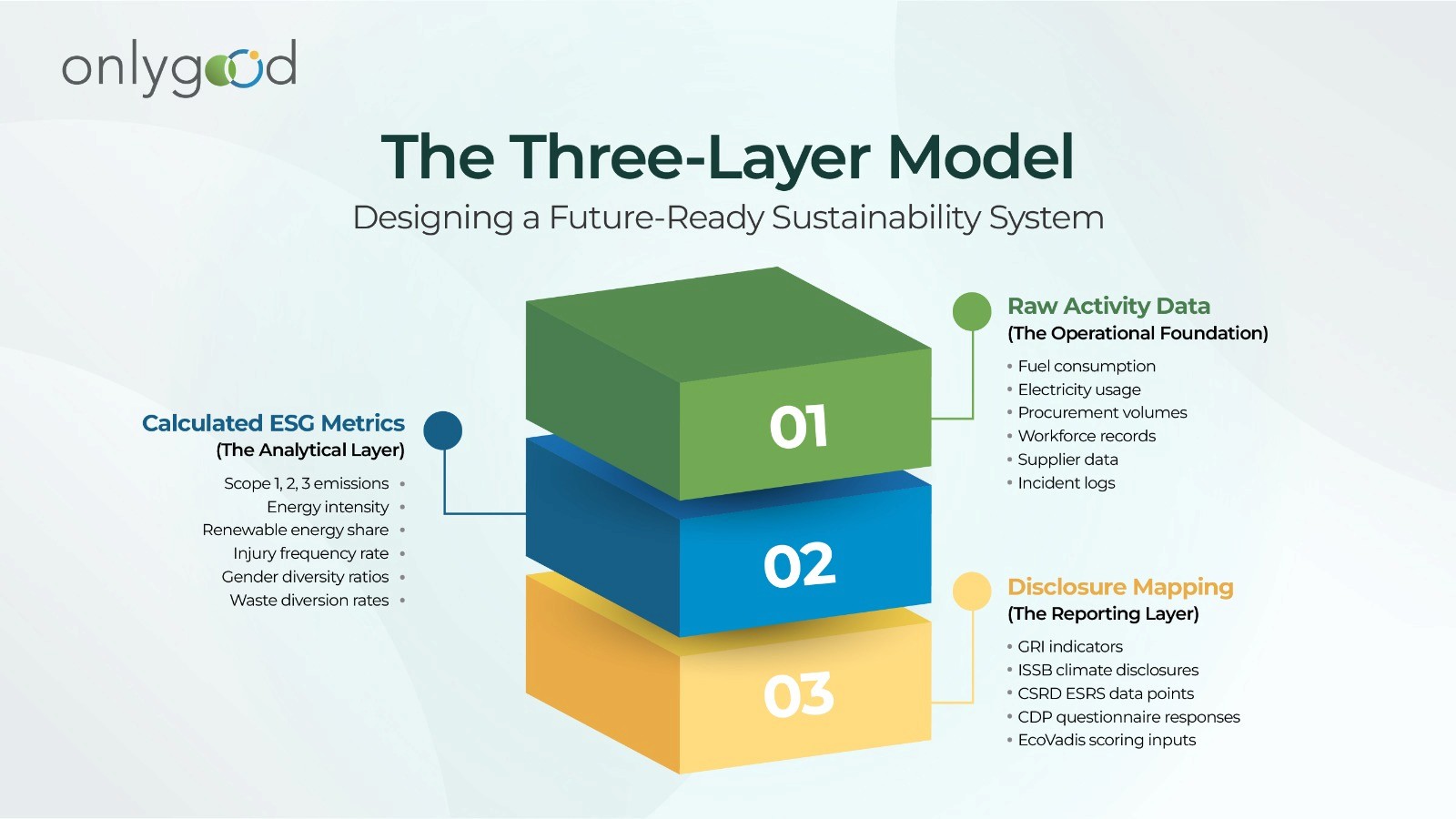

The Three-Layer Model

To design this properly, it helps to think in three layers:

Layer 1: Raw Activity Data

Fuel consumption

Electricity usage

Procurement volumes

Workforce records

Supplier data

Incident logs

Layer 2: Calculated ESG Metrics

Scope 1, 2, 3 emissions

Energy intensity

Renewable energy share

Injury frequency rate

Gender diversity ratios

Waste diversion rates

Layer 3: Disclosure Mapping

GRI indicators

ISSB climate disclosures

CSRD ESRS data points

CDP questionnaire responses

EcoVadis scoring inputs

Most organizations mix all three layers together especially in spreadsheets.

Future-ready systems keep them distinct.

What the Core Must Include

While frameworks differ in structure, the core dataset typically includes:

Environmental

Scope 1, 2, 3 emissions

Emission factors and calculation boundaries

Energy consumption (by source)

Water withdrawal and discharge

Waste generation and disposal

Renewable energy procurement

Social

Workforce composition (gender, age, category)

Health & safety metrics

Training hours

Employee turnover

Community investment data

Governance

Board oversight structures

ESG risk registers

Policy documentation

Compliance incidents

Ethics reporting mechanisms

These are not framework-specific metrics.

They are foundational sustainability parameters.

Governance Is as Important as Data

A core ESG dataset is only as strong as its governance.

That means:

Defined data owners across departments

Clear calculation methodologies

Version control

Audit trails

Documentation of assumptions

Alignment with Scope 3 reporting boundaries

Integration with double materiality processes

As CSRD readiness increases and assurance requirements tighten, documentation becomes as critical as the number itself.

Why This Approach Reduces Complexity

When the core dataset is centralized and governed:

Scope 3 reporting becomes consistent across disclosures

Double materiality assessments draw from structured data

Investor inquiries use the same verified metrics

Sustainability scoring inputs remain aligned year to year

New frameworks no longer trigger new data hunts. They trigger mapping exercises.

That distinction changes everything.

From Reporting Exercise to Data System

The real transformation is psychological as much as operational.

Instead of asking: “What does this new sustainability framework require?”

The organization asks: “Does our core ESG dataset already capture this parameter?”

If yes - it is a formatting task.

If no - it is a data governance gap to close once, not repeatedly.

That is the foundation of scalable, audit-ready ESG reporting.

And it is the prerequisite for turning sustainability from reactive compliance into strategic intelligence.

Turning One Dataset into Many Reports

Once a governed core sustainability dataset is in place, the nature of ESG reporting changes fundamentally.

The question is no longer how to comply with GRI, ISSB, CSRD, SASB, CDP, or BRSR individually.

The question becomes:

How do we map our verified ESG data to different disclosure formats efficiently and consistently?

Reporting as a Mapping Exercise

Every sustainability framework ultimately requires structured disclosure across governance, strategy, risk, and metrics. When the underlying ESG data is centralized and controlled, reporting becomes a translation layer rather than a reconstruction effort.

For example:

The same Scope 1 and Scope 2 emissions dataset can feed GRI climate disclosures, ISSB climate reporting, CSRD ESRS E1, and CDP submissions.

A single double materiality assessment can inform CSRD compliance, investor communication, and internal risk governance.

Workforce diversity metrics can populate GRI disclosures, BRSR tables, and sustainability scoring platforms.

The number does not change.

Only the presentation does.

The Role of Framework Mapping

To operationalize this, organizations need a structured framework mapping matrix - a crosswalk that links:

Core ESG metrics

→ Framework-specific disclosure requirements

→ Reporting templates and narrative formats

This mapping layer ensures:

No duplication of data collection

Consistent boundaries across reports

Faster disclosure preparation

Reduced audit risk

Without it, companies repeatedly reinterpret definitions and risk misalignment between sustainability reports, annual reports, and regulatory filings.

Why Consistency Matters More Than Volume

Investors and regulators increasingly compare disclosures across time and across peers. Inconsistent metrics especially in Scope 3 reporting undermine credibility.

A unified ESG dataset ensures:

Year-on-year comparability

Transparent documentation of methodology

Alignment between financial and non-financial reporting

Stronger assurance readiness

This consistency directly improves sustainability scoring outcomes and investor confidence.

From Annual Panic to Continuous Reporting

When sustainability reporting is driven by disconnected spreadsheets, every disclosure cycle feels urgent.

When reporting is driven by a structured ESG data system:

Data collection becomes continuous

Monitoring replaces scrambling

Updates are incremental

Assurance becomes manageable

This mirrors the evolution finance underwent decades ago moving from periodic reconciliations to integrated accounting systems.

Sustainability reporting is undergoing the same transformation.

Preparing for the Next Framework Before It Arrives

The regulatory environment will continue to evolve. CSRD requirements may expand. ISSB standards may deepen. Jurisdictional mandates will increase. Scope 3 reporting expectations will tighten.

Organizations that treat reporting as a data mapping exercise are inherently adaptable.

A new sustainability framework does not require starting over.

It requires reviewing whether the existing ESG dataset captures any new parameters and updating the mapping layer accordingly.

That is how companies move from compliance management to reporting resilience.

And it sets the stage for the next shift: using sustainability data not just to report but to benchmark, score, and improve performance strategically.

From Reporting to Readiness: Using Data for Scoring and Action Plans

Once a company has a governed core sustainability dataset and a structured mapping system, reporting stops being the end goal.

It becomes the starting point.

This is where ESG reporting evolves into sustainability readiness.

Reporting Tells You What Happened.

Readiness Tells You What to Do Next.

Most organizations treat sustainability disclosures as output documents, annual reports, CSRD filings, CDP submissions, and investor decks.

But when ESG data is centralized and continuously monitored, it becomes a decision-making tool.

The same data used for:

Scope 3 reporting

Double materiality assessments

Governance disclosures

can also power:

Sustainability scoring

Benchmark comparisons

Target tracking

Decarbonisation planning

Supplier engagement strategies

In other words, reporting data becomes performance intelligence.

The Role of Sustainability Scoring

Scoring mechanisms whether internal scorecards or external platforms translate ESG metrics into comparative signals.

They answer questions such as:

How does our emissions intensity compare to peers?

Is our governance structure aligned with investor expectations?

Are we lagging in supplier transparency?

Are our diversity metrics improving year over year?

When data is fragmented, scoring becomes reactive. When data is governed, scoring becomes diagnostic.

It highlights gaps early before regulatory scrutiny or investor pressure escalates.

Closing the Loop: Data → Insight → Action

A future-ready ESG system should create a feedback loop:

Collect and validate sustainability data

Map to reporting frameworks

Benchmark against peers and standards

Identify gaps and improvement areas

Implement targeted action plans

Monitor progress continuously

For example:

Weak Scope 3 reporting visibility may trigger supplier data integration initiatives.

Underperformance in governance metrics may prompt board-level restructuring.

Gaps identified through double materiality analysis may reshape strategic priorities.

This moves ESG from compliance reporting to strategic planning.

Building Climate and Regulatory Resilience

As CSRD readiness becomes mandatory for more companies and ISSB-aligned investor expectations deepen, regulators will increasingly assess not just disclosure completeness but transition credibility.

Companies will be asked:

Are targets science-aligned?

Is there evidence of progress?

Are risks integrated into financial planning?

A structured ESG data system enables credible answers.

Without it, reporting remains descriptive.

With it, reporting becomes defensible and forward-looking.

The Strategic Shift

Organizations that treat sustainability reporting as an annual obligation remain in reactive mode.

Organizations that treat ESG data as a managed, governed asset gain:

Faster response to regulatory changes

Stronger sustainability scoring outcomes

Improved investor confidence

Clearer decarbonisation roadmaps

Greater internal alignment

At that point, sustainability is no longer a compliance exercise.

It becomes an operational capability.

And that capability defines what truly future-ready sustainability reporting looks like.

What a Future-Ready Sustainability Reporting System Looks Like

If the past decade was about responding to sustainability frameworks, the next decade will be about building systems that anticipate them.

A future-ready sustainability reporting system is not defined by how many reports a company publishes. It is defined by how resilient, integrated, and adaptable its ESG data architecture is.

1. Continuous, Not Annual, ESG Accounting

Traditional ESG reporting operates in cycles of annual data calls, last-minute reconciliations, and deadline-driven disclosures.

A future-ready system operates continuously.

Emissions data is tracked monthly or quarterly

Scope 3 reporting is integrated into procurement workflows

Workforce metrics are synced with HR systems

Governance updates are documented in real time

This mirrors financial reporting evolution from periodic bookkeeping to integrated enterprise systems.

Sustainability accounting must follow the same path.

2. Integrated Scope 3 and Value Chain Visibility

As regulatory expectations expand, especially under CSRD and investor-aligned ISSB disclosures, Scope 3 reporting will remain the most complex area.

Future-ready systems:

Embed supplier data collection into onboarding processes

Standardize emission factor methodologies

Track value chain risks alongside financial risk

Maintain traceable documentation for assurance

Scope 3 cannot be treated as an annual estimation exercise. It must become part of operational data governance.

3. Built-In Double Materiality Workflows

With CSRD readiness requirements emphasizing double materiality, companies need structured mechanisms to assess both:

Financial materiality (risk to enterprise value)

Impact materiality (impact on society and environment)

Future-ready systems:

Maintain dynamic materiality matrices

Document stakeholder engagement processes

Link material risks to KPIs and targets

Align disclosures directly to strategy

This ensures materiality is not a static report appendix but a living governance tool.

4. Audit-Ready, Documented, and Traceable

Assurance requirements are expanding globally. Regulators and investors increasingly demand verification.

Future-ready sustainability reporting includes:

Defined data owners

Clear calculation methodologies

Version-controlled documentation

Evidence trails for Scope 1, 2, and Scope 3 reporting

Alignment between financial and non-financial disclosures

In this model, assurance is not a disruption.

It is a validation step.

5. Flexible Mapping to Evolving Frameworks

The regulatory landscape will continue to change.

New sustainability frameworks will emerge.

Existing standards will deepen.

Sector-specific disclosures will expand.

A future-ready system separates:

Core ESG data from Disclosure formatting layers.

When a new reporting requirement appears, the organization does not start from scratch. It evaluates whether the parameter already exists in the dataset and adjusts the mapping logic accordingly.

Adaptability becomes structural not reactive.

6. ESG as Strategic Infrastructure

Ultimately, a future-ready sustainability reporting system is not just about compliance efficiency.

It enables:

Capital market credibility

Stronger sustainability scoring outcomes

Data-driven decarbonisation strategies

Improved risk governance

Cross-functional alignment

At this stage, ESG reporting ceases to be a burden.

It becomes infrastructure as fundamental to corporate resilience as finance, operations, or risk management.

And once sustainability becomes infrastructure, companies no longer chase frameworks.

They outgrow them.

Moving From Compliance Fatigue to Confidence

The conversation around ESG reporting often begins with pressure.

New sustainability frameworks.

Expanding CSRD readiness requirements.

Deeper Scope 3 reporting scrutiny.

Intensifying investor expectations.

Higher sustainability scoring thresholds.

For many organizations, this creates a constant sense of acceleration more disclosures, more data calls, more audits.

This is compliance fatigue.

But fatigue is not caused by ambition. It is caused by fragmentation.

From Framework Chasing to System Ownership

Companies trapped in reactive reporting ask:

What does this new regulation require?

Which team owns this data point?

How do we reconcile inconsistencies?

Can we meet the deadline?

Companies that build a governed ESG data architecture ask a different set of questions:

Is this parameter already captured in our core dataset?

Does our double materiality assessment reflect emerging risks?

How does our Scope 3 reporting compare with peers?

Where do we improve next year?

The shift is subtle but profound.

One approach is defensive.

The other is strategic.

Confidence Comes From Control

Confidence in sustainability reporting does not come from publishing thicker reports.

It comes from:

Consistent metrics across disclosures

Documented methodologies

Clear governance oversight

Transparent assumptions

Verifiable audit trails

When ESG data is centralized, structured, and continuously monitored, organizations gain:

Predictability in reporting cycles

Faster response to new sustainability frameworks

Stronger investor communication

Improved sustainability scoring outcomes

Reduced regulatory risk

In short, they gain control.

Reframing the Role of Sustainability

At its most mature stage, sustainability reporting is no longer a compliance function.

It becomes:

A risk management system

A capital market signal

A strategy validation mechanism

A long-term value creation tool

This reframing aligns ESG with enterprise resilience rather than regulatory survival.

The Strategic Imperative

The global sustainability landscape will continue to evolve. Frameworks will multiply, merge, and mature. Scope 3 reporting expectations will deepen. Assurance will expand. Regulatory scrutiny will intensify.

Organizations cannot control that evolution.

But they can control their architecture.

The future of sustainability reporting does not belong to companies that master individual frameworks.

It belongs to companies that build systems capable of absorbing them.

When the data layer is strong, new standards become manageable.

When governance is structured, double materiality becomes strategic insight.

When reporting is continuous, deadlines lose their power.

That is the journey from compliance fatigue to confidence.

And it begins not with another framework but with a common core.

Conclusion: From Fragmentation to a Common Core

Sustainability reporting has entered a new era.

What began as voluntary ESG disclosure has evolved into a dense ecosystem of sustainability frameworks, regulatory mandates, investor expectations, and scoring platforms. CSRD readiness, ISSB alignment, expanding Scope 3 reporting, and increasing assurance requirements have elevated the stakes.

The instinctive response has been to manage each requirement individually. But the future does not belong to organizations that chase frameworks.

It belongs to those that recognize a deeper truth:

The complexity of ESG reporting is not primarily a standards problem. It is a systems problem.

Across GRI, SASB, TCFD, ISSB, CSRD, CDP, and national regulations, the overlap at the data layer is significant. Governance structures, emissions metrics, workforce indicators, risk registers, and supply chain transparency form a shared sustainability architecture.

When companies build a governed, audit-ready core sustainability dataset:

Scope 3 reporting becomes consistent and defensible

Double materiality becomes structured and strategic

Sustainability scoring becomes diagnostic rather than reactive

New frameworks become mapping exercises, not transformation projects

This is the shift from reactive compliance to future-ready sustainability reporting.

The organizations that thrive in this environment will not be those with the longest sustainability reports but those with the strongest ESG data foundations.

In a world of 600+ frameworks and growing regulatory convergence, the competitive advantage lies in simplicity at the core.

One governed dataset.

Many reporting outputs.

Continuous insight.

That is how companies move from compliance fatigue to confidence and from fragmented disclosure to resilient sustainability leadership.