Introduction: India’s Carbon Moment

For decades, carbon emissions sat quietly in the background of India’s growth story unmeasured, unpriced, and largely unquestioned. Today, that era is decisively over. Carbon is no longer an abstract environmental concern; it is measured, tracked, regulated, and increasingly monetised.

What was once a peripheral sustainability issue has moved into the core of business strategy, trade competitiveness, and national policy.

Globally, ESG has crossed a critical threshold. Sustainability is now embedded in regulation, capital allocation, and cross-border trade. Mechanisms like the EU’s Carbon Border Adjustment Mechanism (CBAM), mandatory climate disclosures, and investor-led scrutiny are forcing companies to account for emissions not just within their operations, but across entire value chains. Carbon has become a filter for market access.

India now finds itself at a defining inflection point. Between 2025 and 2035, the country must balance rapid economic expansion with growing climate accountability. With its net-zero commitment for 2070, the launch of a domestic carbon market framework, and rising pressure on exporters and suppliers, India is transitioning from intent to implementation.

This moment marks a deeper shift from carbon ignorance to carbon intelligence. Businesses are being pushed to understand emissions not as an unavoidable by-product of growth, but as a quantified variable that influences cost, risk, and opportunity.

How India responds in this decade will determine whether carbon becomes a constraint or a strategic lever for sustainable growth.

What Do We Mean by “Carbon Culture”?

Carbon culture reflects how an economy, its institutions, and its businesses understand, value, and respond to emissions. Regulation may set the rules, but culture determines how seriously those rules are taken.

At the business level, carbon culture shapes perception.

Is carbon viewed as an invisible by-product of operations, or as a measurable variable that influences efficiency, cost, and competitiveness?

Companies with mature carbon cultures do not ask if emissions must be measured, but how accurately and how early they can act on that data.

Equally critical is the role of data integrity. A strong carbon culture treats emissions data with the same discipline as financial data auditable, traceable, and decision-ready. Weak cultures rely on estimates, averages, and assumptions, increasing exposure to regulatory risk and market penalties.

Most importantly, carbon culture defines intent.

Carbon can be treated purely as a compliance cost, reluctantly managed to meet minimum requirements. Or it can be approached as a strategic lever one that unlocks access to capital, protects export competitiveness, and enables long-term value creation.

India’s evolving carbon journey is ultimately a story of this cultural shift.

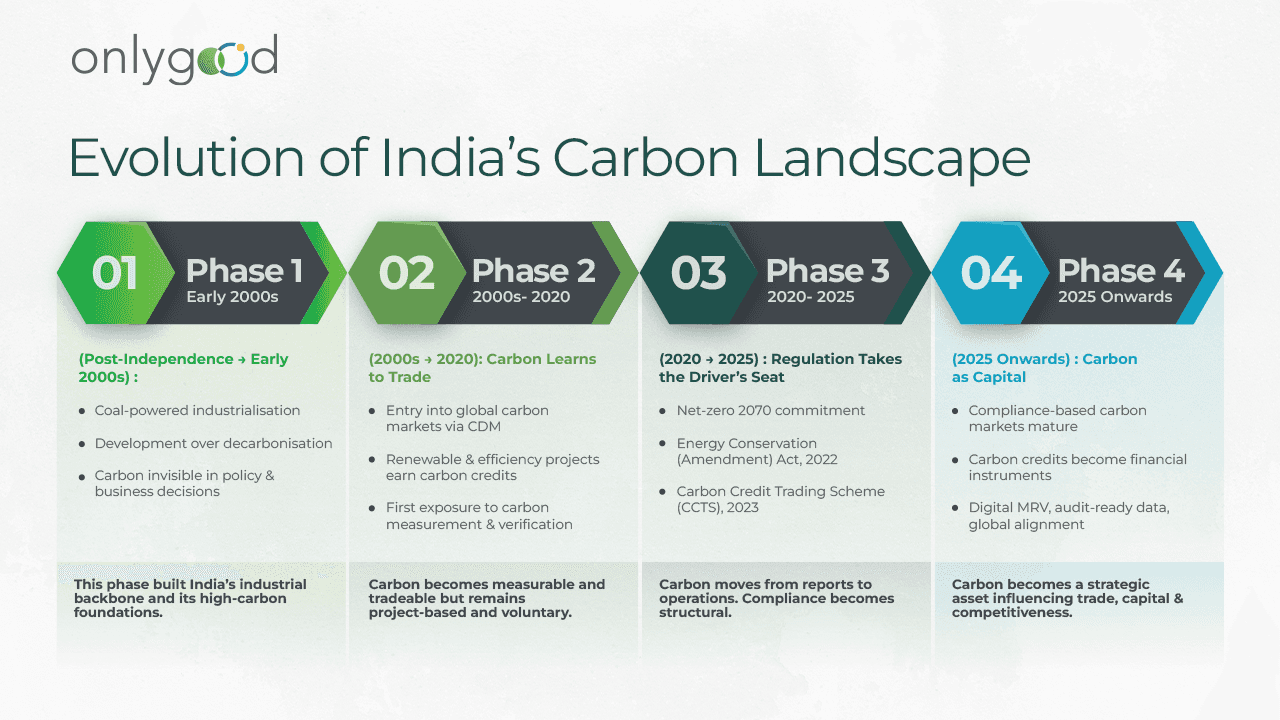

Phase 1: Post-Independence to the Early 2000s - Growth First, Carbon Later

In the decades following independence, India’s economic priorities were unambiguous. The country faced the urgent task of industrialisation, poverty alleviation, and energy security for a rapidly growing population. In this context, coal emerged not as a choice, but as a necessity—abundant, domestically available, and capable of powering large-scale development.

Carbon emissions, during this phase, were largely invisible in public discourse and business decision-making. The idea of measuring or pricing emissions held little relevance in an economy focused on building factories, expanding infrastructure, and achieving self-reliance. Environmental regulation, where it existed, was aimed at local pollution and resource use rather than climate impact. Carbon, as a concept, remained distant and abstract.

This period shaped India’s early carbon culture in a fundamental way. Emissions were seen as an unavoidable by-product of growth—an externality to be addressed later, once development goals were met. Unlike advanced economies that began industrialising earlier and could afford to externalise emissions for longer, India was still establishing its economic base when global climate conversations began to take shape.

Crucially, there was no international pressure and no domestic incentive to account for carbon. Global climate agreements were either absent or non-binding, and Indian businesses faced no commercial disadvantage for being carbon-intensive.

This high-carbon development phase laid the structural foundations of energy systems, industrial clusters, and supply chains that continue to influence India’s emissions profile today. It also explains why India’s transition toward carbon accountability would later need to be gradual, intensity-focused, and growth-sensitive, rather than abrupt or absolute.

Phase 2: 2000s to 2020 - The Clean Development Mechanism (CDM) Era

The early 2000s marked India’s first meaningful engagement with carbon markets. With the adoption of the Kyoto Protocol, carbon entered the Indian policy and business vocabulary through the Clean Development Mechanism (CDM). For the first time, emissions reductions were assigned economic value, allowing developing countries like India to generate carbon credits by implementing cleaner technologies.

India quickly emerged as one of the world’s largest CDM participants. Renewable energy projects, waste heat recovery, and energy efficiency initiatives particularly in wind, hydro, and industrial sectors were registered under international standards such as the UNFCCC, Verra, and Gold Standard. For many Indian companies, carbon credits represented a new revenue stream, often improving the financial viability of projects that might otherwise have struggled to secure funding.

This period played a critical educational role. It introduced Indian businesses to baseline calculations, monitoring methodologies, verification processes, and third-party audits. Carbon, for the first time, became measurable and tradeable.

However, the CDM era had structural limitations. Participation was project-based and voluntary, not economy-wide. Carbon management remained siloed—handled by sustainability consultants or project teams rather than integrated into core business strategy. Most companies viewed carbon credits as an add-on benefit, not as a signal to fundamentally rethink emissions across operations.

More importantly, CDM did little to build a broad carbon culture. It created carbon projects, but not carbon-conscious organisations. Emissions outside registered projects remained largely unmeasured, and supply chains were untouched. When global demand for CDM credits weakened after 2012, carbon activity in India slowed sharply revealing its dependence on external markets rather than domestic policy.

Still, this phase laid essential groundwork. The Energy Conservation Act of 2001 and the later Perform, Achieve and Trade (PAT) scheme began shifting focus toward domestic energy efficiency and performance benchmarking. Together, these initiatives quietly prepared India for its next transition from voluntary participation to regulatory responsibility.

The CDM era was not a failure; it was a learning curve. It taught India how carbon could be measured and traded but not yet why it needed to be embedded into mainstream business decision-making.

Phase 3: 2020–2025 - Regulation Takes the Driver’s Seat

The period between 2020 and 2025 marked a decisive shift in India’s carbon journey. What had once been voluntary, fragmented, and externally driven began transforming into a state-led, regulation-backed framework with long-term economic intent. Carbon moved from the margins of sustainability conversations into the centre of policy and industrial planning.

The turning point came at COP26 in Glasgow, where India announced its commitment to achieve net-zero emissions by 2070. While the timeline was longer than that of developed economies, the signal was unambiguous: carbon would now be governed, measured, and progressively priced. This declaration was followed by concrete domestic action.

The Energy Conservation (Amendment) Act, 2022 fundamentally altered India’s approach to emissions management. For the first time, the government was empowered to establish a domestic carbon market, moving beyond energy efficiency metrics to direct emissions accountability. This shift acknowledged a critical reality: energy savings alone were no longer sufficient in a world increasingly focused on absolute and intensity-based emissions reduction.

In June 2023, the Carbon Credit Trading Scheme (CCTS) was formally notified, signalling India’s transition toward a compliance-oriented carbon market. Unlike the project-based CDM framework, the CCTS is designed as a cap-and-trade system, initially targeting high-emitting sectors such as power, steel, cement, and refining. Entities are now required to meet specific emissions intensity targets, with carbon credits becoming instruments of compliance rather than optional incentives.

This represented a profound cultural shift for Indian industry. Under earlier regimes like the Perform, Achieve and Trade (PAT) scheme, companies focused on reducing energy consumption per unit of output. Under the emerging carbon market, the focus expands to measuring and managing actual emissions, integrating fuel mix, process efficiency, and operational decisions.

Crucially, the CCTS aligns with India’s development priorities. By emphasising emissions intensity rather than absolute caps, the framework allows economic growth while steadily improving carbon efficiency. This approach reflects India’s unique challenge: decarbonising without deindustrialising.

For businesses, the implications are immediate and structural. Carbon data must now be accurate, verifiable, and increasingly audit-ready. Compliance is no longer limited to large emitters; pressure is cascading through value chains as customers, financiers, and regulators demand transparency. Carbon management is becoming a strategic function, intersecting operations, finance, procurement, and risk management.

This phase marks India’s transition from carbon participation to carbon governance, a necessary foundation for the more complex, market-driven carbon economy that lies ahead.

Phase 4: 2025 Onwards - Carbon as Capital

From 2025 onward, India’s carbon journey enters its most consequential phase. Carbon is no longer treated merely as an environmental externality or a compliance obligation; it begins to function as capital: measurable, tradeable, and strategically valuable.

At the heart of this transition is the maturation of India’s domestic carbon market under the Carbon Credit Trading Scheme (CCTS). As sectoral coverage expands and emissions baselines become more robust, carbon credits evolve into financial instruments that reward efficiency, innovation, and early action. Companies that invest in cleaner technologies, process optimisation, and credible data systems stand to generate surplus credits turning emissions reduction into a balance-sheet advantage rather than a sunk cost.

This phase also coincides with rapid digitalisation of carbon infrastructure. The future of carbon markets depends heavily on trust, traceability, and integrity. To address this, India is seeing early adoption of digitally verified carbon offsets, supported by AI-driven measurement, reporting, and verification (MRV) systems, as well as blockchain-based registries. These tools reduce the risk of double counting, improve auditability, and increase market confidence critical factors as carbon trading volumes rise.

Simultaneously, India is aligning its carbon framework with Article 6 of the Paris Agreement, opening pathways for international carbon trading through Internationally Transferred Mitigation Outcomes (ITMOs). This integration has the potential to position India as a major supplier of high-integrity carbon credits to global markets, particularly as demand rises from regions facing stringent border regulations such as the EU’s Carbon Border Adjustment Mechanism (CBAM).

The concept of carbon capital is also reshaping sub-national and urban strategies. Cities and states are beginning to recognise carbon efficiency as an economic lever—driving investment, improving competitiveness, and attracting climate finance. Emerging hubs, including Indore, are being cited for their proactive engagement with carbon accounting, waste-to-energy projects, and tradable credit mechanisms.

However, this future is not without friction. Compliance costs, especially for MSMEs, remain a significant challenge. Without accessible tools, simplified reporting frameworks, and ecosystem support, smaller enterprises risk exclusion from carbon markets altogether. Equally critical is the need to maintain high credit quality. As markets scale, ensuring integrity and avoiding greenwashing will determine whether India’s carbon economy earns global credibility or faces regulatory pushback.

Ultimately, this phase represents a redefinition of value. Carbon is no longer just something to reduce, it is something to manage intelligently, price accurately, and deploy strategically. Businesses that recognise this shift early will not only stay compliant but shape India’s low-carbon growth story.

Key Drivers Accelerating India’s Carbon Culture Shift

India’s evolving carbon culture is not happening in isolation. It is being accelerated by a powerful mix of external pressure and internal ambition, where global trade realities meet domestic economic priorities.

1. Global Trade Is Now Carbon-Gated

The single biggest external trigger is the EU’s Carbon Border Adjustment Mechanism (CBAM). For carbon-intensive Indian exports; steel, cement, aluminium, fertilizers carbon disclosure is no longer optional. Emissions data now directly influences market access, pricing power, and competitiveness. Similar border-linked mechanisms are being discussed across the UK, Japan, and parts of North America, signalling a future where carbon transparency becomes a prerequisite for global trade.

In this world, carbon ignorance is costly.

2. Capital Is Following Carbon Intelligence

Investors are increasingly pricing climate risk into valuations. Indian companies seeking global capital through bonds, equity, or project finance are facing sharper scrutiny on emissions intensity, transition plans, and data credibility. ESG-linked loans, sustainability-linked bonds, and climate funds all demand verifiable carbon metrics, not narrative intent. Carbon is becoming a language of capital allocation.

3. National Growth Meets Climate Accountability

India’s ambition to become a $5 trillion economy while committing to net-zero by 2070 requires a delicate balance. Instead of absolute emission cuts, India’s focus on emissions intensity reduction allows growth but only if efficiency improves. This makes carbon measurement a strategic necessity, not a moral choice.

4. Supply Chains Are Under the Microscope

Large corporations can no longer decarbonise in isolation. Scope 3 emissions often 60–80% of total footprints force companies to look downstream and upstream. Suppliers are now being pulled into carbon reporting ecosystems, reshaping how MSMEs engage with sustainability. What began as corporate ESG is rapidly becoming supply-chain ESG.

Together, these drivers are transforming carbon from a background concern into a core business variable one that influences trade, finance, reputation, and long-term resilience.

What This Means for Indian Businesses: Winners, Laggards, and the Cost of Delay

India’s carbon transition will not impact all businesses equally. The emerging carbon economy is already creating clear winners and exposed laggards, with the gap widening rapidly as regulation, capital, and supply-chain expectations converge.

1. The Winners: Carbon-Ready Businesses

Forward-looking companies are treating carbon as a strategic asset, not a compliance headache. These organisations have begun measuring Scope 1 and 2 emissions consistently, engaging suppliers on Scope 3 data, and embedding carbon intelligence into operational decisions energy sourcing, process efficiency, logistics, and procurement.

For them, sustainability delivers tangible upside:

Easier access to global customers and export markets

Preferential treatment from investors and lenders

Stronger negotiating power with OEMs and multinationals

Faster readiness for India’s upcoming compliance-based carbon market

These businesses will not scramble when disclosure becomes mandatory; they will already be positioned ahead of the curve.

2. The Laggards: Reactive and Unprepared

On the other side are companies delaying action, assuming ESG is either optional or someone else’s responsibility. Many MSMEs still view carbon reporting as paperwork rather than infrastructure. The risk here is not just regulatory penalties, it is commercial exclusion.

As large buyers tighten ESG requirements, suppliers unable to provide credible emissions data risk losing contracts, facing pricing pressure, or being replaced altogether.

3. The Cost of Delay

The most dangerous position is in-between: businesses that intend to act “later.” Carbon capability takes time data systems, internal alignment, supplier engagement, and verification cannot be built overnight. Delayed action compounds costs, limits options, and reduces strategic flexibility.

In India’s emerging carbon economy, early movers gain leverage, while late adopters pay premiums financial, operational, and reputational.

Carbon readiness is no longer about doing good. It is about remaining relevant.

India’s Carbon Market Architecture: From Efficiency Targets to Carbon Trading

India’s carbon journey has not followed the dramatic “cap-first” models seen in Europe or parts of North America. Instead, it has evolved through a gradual, system-building approach, designed to balance climate action with economic growth. Understanding this architecture is critical for businesses preparing for what comes next.

1. The PAT Scheme: Training Ground for Carbon Discipline

Launched in 2012 under the National Mission for Enhanced Energy Efficiency, the Perform, Achieve and Trade (PAT) scheme was India’s first large-scale market mechanism addressing emissions indirectly. Rather than pricing carbon, it set specific energy consumption targets for energy-intensive industries such as steel, cement, power, aluminium, and fertilisers.

While PAT focused on energy efficiency, it quietly built India’s foundational carbon muscle:

Measurement and verification systems

Plant-level data reporting discipline

Tradeable certificates (ESCerts) as a market signal

For many Indian manufacturers, PAT was their first exposure to compliance-driven sustainability.

2. The Shift from Energy to Emissions

As global climate expectations intensified, energy efficiency alone proved insufficient. What mattered increasingly was absolute and intensity-based emissions, especially for export-facing industries exposed to mechanisms like the EU’s CBAM.

This led to a structural rethink.

3. The Carbon Credit Trading Scheme (CCTS)

Notified in 2023, the Carbon Credit Trading Scheme (CCTS) marks India’s formal transition toward a national, compliance-based carbon market. Unlike voluntary offset markets, CCTS introduces a regulated framework where emissions performance carries direct economic consequences.

Key design signals:

Focus on emissions intensity, not absolute caps

Gradual sectoral onboarding

Alignment with India’s growth and net-zero pathways

In effect, CCTS transforms carbon from a reporting metric into a priced operational variable.

India is no longer experimenting. It is institutionalising carbon.

Global Pressure Meets Domestic Policy: Why This Shift Is Happening Now

India’s acceleration toward a formal carbon market is not happening in isolation. It is being shaped by a powerful convergence of global trade rules, investor expectations, and geopolitical climate policy.

1. Carbon Has Become a Trade Barrier

Mechanisms like the EU Carbon Border Adjustment Mechanism (CBAM) have fundamentally altered how carbon is viewed in international commerce. For the first time, emissions embedded in products such as steel, cement, aluminium, and fertilisers directly affect export competitiveness.

For Indian exporters, this has two immediate implications:

Emissions data must be accurate, auditable, and product-linked

Carbon intensity now influences pricing, margins, and market access

2. Investors and Lenders Are Raising the Bar

Global capital is increasingly governed by ESG-linked risk models. Banks, private equity, and institutional investors now assess carbon exposure alongside financial performance. Companies without credible emissions data face:

Higher cost of capital

Limited access to global funding

Increased scrutiny in M&A and supply chain partnerships

This is especially relevant for Indian firms integrated into multinational value chains.

3. Policy Alignment, Not Imitation

India’s response is not a copy-paste of Western climate policy. Instead, it reflects a strategic alignment absorbing global expectations while preserving domestic growth priorities. The emphasis on emissions intensity, phased compliance, and sectoral readiness reflects this balance.

The result is a uniquely Indian model:

globally interoperable, domestically calibrated, and growth-conscious.

The next decade will determine whether businesses adapt early or absorb the cost later.

From Voluntary ESG to Mandatory Carbon Accountability

For over a decade, sustainability in India largely lived in the realm of voluntary action—CSR disclosures, sustainability reports, and selective participation in global frameworks. Carbon reporting, where it existed, was often high-level, estimated, and driven more by reputation than regulation. That era is ending.

Today, carbon accountability in India is moving decisively from choice to obligation.

1. Regulation Is Becoming Operational

With the Energy Conservation (Amendment) Act, 2022 and the notification of the Carbon Credit Trading Scheme (CCTS) in 2023, emissions management is no longer confined to reporting. It is becoming target-based, measurable, and enforceable. Sectors such as steel, cement, power, and refining are transitioning from energy-efficiency benchmarks to emissions intensity targets, directly linking performance to compliance outcomes.

This marks a critical shift: carbon data will no longer sit in annual reports; it will influence day-to-day operational decisions.

2. Reporting Is Becoming Transactional

Carbon information is now required at the transaction level by customers, financiers, and regulators. Exporters face CBAM declarations. Large enterprises demand Scope 1 and Scope 2 data from suppliers to calculate their Scope 3 exposure. Inaccurate or delayed data increasingly translates into lost contracts or delayed shipments.

3. Accountability Is Moving Down the Value Chain

Perhaps the most significant change is where responsibility sits. Carbon accountability is no longer limited to large corporations. MSMEs, suppliers, and contract manufacturers are now part of the compliance equation whether prepared or not.

This shift signals the rise of carbon as a core business parameter, not a sustainability add-on.

The Cultural Shift Ahead: From Compliance to Carbon Intelligence

India is now entering the most important phase of its carbon journey—not one driven by new rules alone, but by a deeper cultural shift in how carbon is understood and managed inside businesses.

For years, carbon compliance meant meeting minimum thresholds: filing disclosures, submitting energy data, or participating in efficiency schemes like PAT. Carbon was treated as a reporting obligation static, backward-looking, and largely siloed within sustainability teams.

That approach is no longer sufficient.

As carbon markets mature and global trade mechanisms like CBAM begin to penalize opacity, carbon is becoming a strategic data asset. Forward-looking companies are shifting from carbon compliance to carbon intelligence, the ability to measure, verify, analyze, and act on emissions data in near real time.

This shift changes the business conversation entirely. Carbon data now influences procurement decisions, supplier selection, capital access, and export competitiveness. Emissions are no longer an abstract environmental metric; they are operational inputs that affect margins, pricing power, and risk exposure.

Crucially, this cultural shift also reframes carbon from being only a cost or risk to being an opportunity. Companies with high-quality emissions data can optimize processes, unlock efficiency gains, access green finance, and participate credibly in domestic and international carbon markets. Those without it face default values, border penalties, delayed shipments, and eroding trust.

India’s emerging carbon culture, therefore, is not about doing “more sustainability.” It is about doing better business with better data where carbon intelligence becomes as fundamental as financial accounting or quality control.

Conclusion: India’s Carbon Decade

Carbon in India is no longer invisible, unpriced, or negotiable.

It is being measured, regulated, and increasingly traded. It is shaping access to global markets, influencing capital flows, and redefining what credible growth looks like in a carbon-constrained world. ESG, once voluntary and reputational, is now structural.

The decade from 2025 to 2035 will determine whether India emerges as a competitive, low-carbon manufacturing and services powerhouse or struggles with rising trade barriers, fragmented compliance, and reactive transitions. Policy signals are clear, markets are aligning, and global expectations are accelerating faster than many businesses anticipate.

In this environment, the divide will not be between sustainable and unsustainable companies, but between early movers and late responders. Those who invest early in emissions data, verification, and internal carbon capabilities will shape standards, secure market access, and unlock long-term resilience. Those who delay will be forced into hurried compliance often at higher cost and lower credibility.

India’s carbon journey has evolved from ignorance to awareness, from offsets to accountability, and now toward intelligence. The question for businesses is no longer whether carbon will matter but whether they will be prepared when it does.

This is India’s carbon decade. The advantage will belong to those who treat carbon not as a burden, but as a strategic reality to be understood, managed, and mastered.