Next Phase of Sustainability Regulation

Global sustainability regulations are entering a new phase of maturity and complexity, one that moves beyond voluntary commitments toward mandatory, enforceable, and deeply integrated compliance. The era of “best-effort sustainability” is ending; the era of “accountable sustainability” has begun.

Across industries and geographies, businesses are now operating under an evolving web of environmental, social, and governance (ESG) mandates that extend far beyond traditional reporting. From Extended Producer Responsibility (EPR) frameworks that redefine waste ownership, to the Carbon Border Adjustment Mechanism (CBAM) that embeds carbon costs directly into international trade, to the Corporate Sustainability Reporting Directive (CSRD) that mandates granular disclosures across supply chains — the message is clear: sustainability is no longer optional or isolated; it is structural.

This next regulatory wave is marked by three defining shifts:

From voluntary to mandatory: Companies can no longer rely on broad sustainability statements; they must provide verified, auditable data to prove their environmental and social performance.

From operations to ecosystems: Regulations now demand visibility across the entire value chain — including suppliers, distributors, and end-of-life processes — forcing companies to build deep traceability into procurement and production.

From compliance to competitiveness: What began as a risk-avoidance exercise has evolved into a strategic differentiator. Businesses that anticipate, adapt, and align early are gaining an edge in markets where sustainability credentials are becoming prerequisites for trade, investment, and reputation.

For global exporters and manufacturers — particularly in emerging markets like India — these shifts carry both challenge and opportunity. The cost of inaction is rising, but so too is the potential to leverage compliance as a driver of innovation, efficiency, and market access.

At Onlygood, we see this transformation not as regulatory pressure, but as a strategic inflection point. The convergence of EPR, CBAM, CSRD, and other ESG frameworks is laying the groundwork for more transparent, accountable, and resilient value chains. Businesses that embrace data-driven sustainability today will not only meet the standards of tomorrow — they will define them.

In essence, the sustainability mandate is evolving from a policy requirement to a performance revolution. The organizations that adapt with foresight, intelligence, and agility will lead in a global economy where compliance, competitiveness, and conscience are finally aligned.

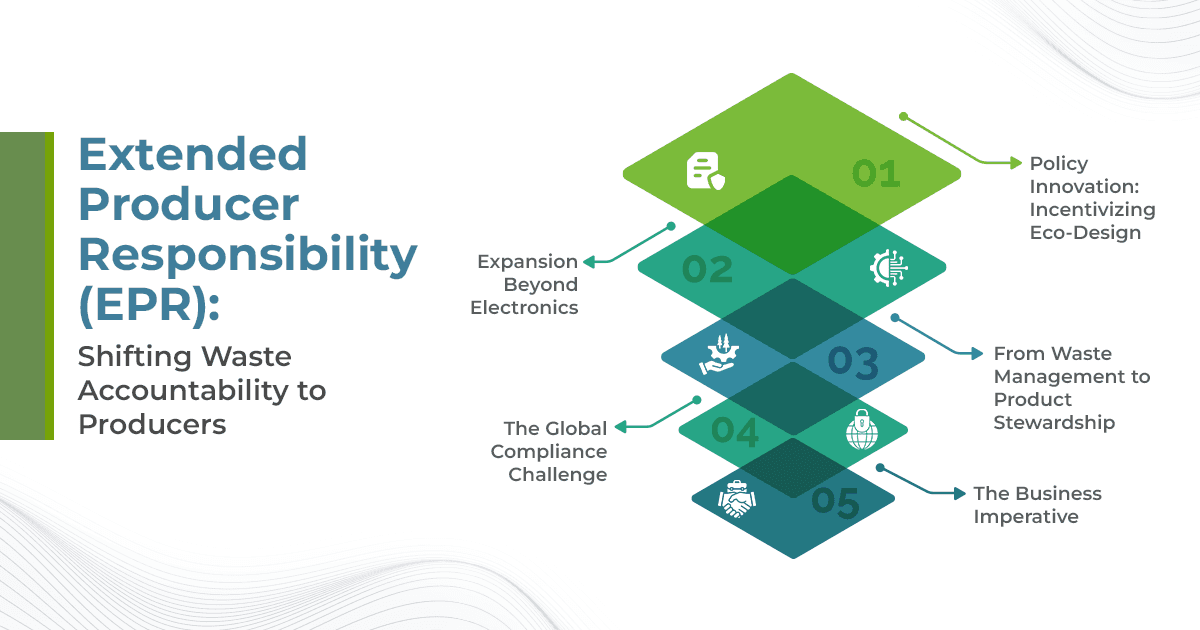

Extended Producer Responsibility (EPR): Shifting Waste Accountability to Producers

The concept of Extended Producer Responsibility (EPR) marks a fundamental shift in how businesses engage with the products they bring to market. No longer limited to the point of sale, accountability now extends to the entire lifecycle of a product — from design and distribution to post-consumer waste management. Under EPR, manufacturers, importers, and brand owners are not only responsible for producing goods efficiently but also for ensuring that those goods can be collected, recycled, or safely disposed of at the end of their use.

From Waste Management to Product Stewardship

Traditionally, the responsibility for managing waste has rested with municipalities and local governments. EPR reverses that model — shifting the burden to producers who are best positioned to design for sustainability. By embedding responsibility at the design and production stages, EPR encourages product stewardship, where environmental impact is minimized before waste is even created.

Expansion Beyond Electronics

What began as a policy framework for e-waste and batteries is now expanding rapidly. In markets such as India and the European Union, EPR has broadened its scope to include plastic packaging, textiles, and multi-layered materials, with ongoing discussions around inclusion of other high-impact categories like construction materials and automotive components. This widening net signals a global transition toward circular economy thinking, where waste is treated as a resource and every product is designed with recovery in mind.

Policy Innovation: Incentivizing Eco-Design

One of the most promising evolutions in EPR policy lies in modulated fee models, such as those adopted in the Netherlands and France. Under these frameworks, producers that design products for easier recyclability or use recycled materials benefit from lower EPR fees, while those that do not face higher charges. This “polluter-pays” model is being refined into a “designer-rewards” model — turning regulation into an innovation incentive.

The Business Imperative

For businesses, EPR compliance is no longer just about waste collection — it’s about data, design, and coordination. Companies must:

Track and report product-level material data across their entire value chain.

Ensure that packaging and products meet recyclability and reuse criteria.

Collaborate with recyclers, waste aggregators, and compliance partners to close the loop.

The success of an EPR strategy now depends on cross-functional alignment between sustainability, product design, supply chain, and compliance teams — supported by robust digital data infrastructure.

The Global Compliance Challenge

However, as more countries roll out their own EPR frameworks, compliance has become increasingly fragmented. Fee structures, reporting templates, and recovery obligations vary widely between regions — from India’s Plastic Waste Management Rules to the EU’s Packaging and Packaging Waste Directive and Canada’s provincial EPR schemes. For global manufacturers, this means managing multiple compliance systems simultaneously, each with its own technical and legal nuances.

The path forward is clear: businesses that treat EPR not as an administrative requirement, but as a design and data opportunity, will be better positioned to lead in a world shifting toward circularity. By embracing digital product passports, lifecycle tracking, and eco-design principles, companies can turn regulatory compliance into a competitive differentiator — aligning profitability with planetary responsibility.

Carbon Border Adjustment Mechanism (CBAM): Redefining Trade Through Carbon Accountability

The European Union’s Carbon Border Adjustment Mechanism (CBAM) represents one of the most significant transformations in global trade policy since the introduction of carbon pricing itself. It is more than a climate policy — it’s an instrument to level the playing field between regions with differing climate ambitions, ensuring that carbon costs are embedded into the true price of global goods.

Why CBAM Exists: Preventing Carbon Leakage

At its core, CBAM is designed to address carbon leakage — the practice of companies shifting production to countries with less stringent climate policies to avoid carbon costs. Such behavior undermines the EU’s climate goals and distorts competition. CBAM corrects this by imposing a carbon-linked cost on imports that mirrors the cost EU manufacturers already bear under the EU Emissions Trading System (ETS).

This approach signals a new era where carbon intensity becomes a tradable factor — one that influences not only competitiveness but also access to markets.

How It Works

Currently in its transitional phase (2023–2025), CBAM requires importers to report the embedded carbon emissions in select products such as cement, steel, aluminum, fertilizers, hydrogen, and electricity.

From 2026 onwards, importers will need to purchase CBAM certificates corresponding to the carbon intensity of their imported goods. These certificates effectively price the emissions generated outside the EU, ensuring that imported products bear the same carbon cost as those produced domestically.

The result is clear: carbon transparency is no longer optional — it is a prerequisite for international trade.

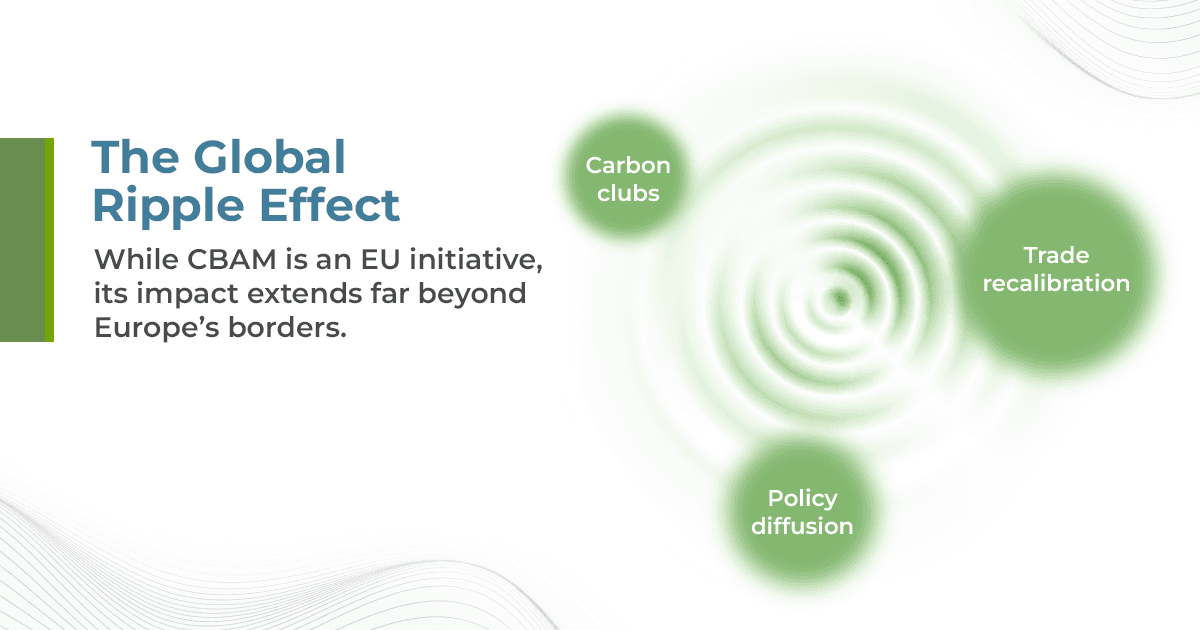

The Global Ripple Effect

While CBAM is an EU initiative, its impact extends far beyond Europe’s borders.

Policy diffusion: Countries like the United Kingdom, Canada, and the United States are exploring similar border carbon mechanisms.

Trade recalibration: Export-oriented economies such as India, China, and Vietnam are reassessing production processes and export strategies to remain competitive.

Carbon clubs: The EU’s move is fostering the creation of alliances among nations with aligned carbon pricing policies, establishing new trade blocs based on sustainability performance.

For exporters, particularly in developing economies, this means that carbon data will soon be as critical as cost and quality in determining global competitiveness.

Business Implications: Data, Strategy, and Supply Chain Transparency

CBAM compliance is not merely a reporting exercise — it demands end-to-end carbon visibility across the supply chain. Businesses must now:

Map carbon emissions from raw materials to final products (Scopes 1–3).

Integrate supplier-level data and digital monitoring systems.

Align procurement and production with low-carbon energy sources.

Establish internal pricing on carbon to anticipate cost pass-throughs.

Firms that build these capabilities early will not only comply but gain a cost advantage, reducing exposure to future carbon tariffs and positioning themselves as preferred suppliers in carbon-conscious markets.

Challenges and Transition Risks

The immediate challenge for many exporters — especially mid-sized and developing-market firms — lies in the data gap. Collecting accurate, verifiable emissions data across fragmented supply chains is complex and resource-intensive. In addition, differences in national carbon accounting standards complicate interoperability.

However, the long-term benefit outweighs the short-term strain. Companies that invest now in digital carbon tracking, lifecycle assessment tools, and supplier engagement will build resilience and market credibility in an increasingly carbon-regulated world.

From Compliance to Competitiveness

CBAM is not just a regulatory hurdle — it is a signal of the future global economy, where carbon performance defines trade access, cost competitiveness, and investor confidence. Forward-thinking companies are already turning compliance into strategy by:

Embedding carbon intelligence into procurement and product design.

Forming partnerships with low-carbon suppliers.

Leveraging technology to automate emissions reporting and verification.

Ultimately, CBAM redefines what it means to be competitive in the 21st century: those who can measure and manage carbon will lead; those who cannot will pay the price — literally.

Beyond EPR and CBAM: The Expanding Web of Global Sustainability Regulations

The global regulatory landscape is entering a new era — one where sustainability is no longer treated as a single policy area but as an integrated framework of environmental, social, and governance (ESG) accountability. EPR and CBAM are only the beginning. The next wave of mandates — from comprehensive ESG disclosures to supply chain due diligence and anti-greenwashing laws — is transforming how companies operate, report, and compete on the world stage.

From Voluntary Reporting to Mandatory Transparency

In the past, corporate sustainability reporting was largely voluntary — driven by reputation, investor expectations, or consumer goodwill. That era is ending. Regulations like the EU’s Corporate Sustainability Reporting Directive (CSRD) and the International Sustainability Standards Board (ISSB) are now making ESG disclosure mandatory, auditable, and comparable across borders.

The CSRD alone will affect nearly 50,000 companies, including non-EU entities with significant operations or subsidiaries in Europe. It requires businesses to disclose detailed information on carbon emissions (including Scope 3), biodiversity, human rights, and governance performance, all in line with standardized European Sustainability Reporting Standards (ESRS).

The ISSB, meanwhile, is establishing a global baseline for sustainability reporting, allowing investors to compare companies across jurisdictions — much like financial reporting today.

Supply Chain Due Diligence: Accountability Beyond Borders

Beyond disclosure, governments are now demanding responsibility across entire value chains. The EU Corporate Sustainability Due Diligence Directive (CSDDD) and similar laws in the U.S. and Germany require companies to identify, prevent, and mitigate environmental and human rights risks in their supplier networks.

This means companies are being held accountable not just for their own emissions or labor practices, but also for those of their contractors, raw material suppliers, and logistics partners. Non-compliance can result in penalties, trade restrictions, or even exclusion from public procurement — signaling that ethical and environmental diligence is now a business license to operate.

Anti-Greenwashing and Marketing Integrity

As sustainability gains prominence, greenwashing — the act of overstating or misrepresenting environmental performance — has come under intense scrutiny. Regulations such as the EU Green Claims Directive and upcoming amendments in India’s Advertising Standards Council guidelines are raising the bar for truth in environmental communication. Brands must now substantiate claims like “eco-friendly,” “biodegradable,” or “net-zero” with verified data and third-party validation.

The message is clear: transparency isn’t just expected; it’s legally required.

Circular Economy Mandates and Product Transparency

Complementing these reporting and disclosure initiatives are new policies promoting circular design and material traceability. The EU’s Ecodesign for Sustainable Products Regulation (ESPR), along with the Digital Product Passport (DPP) initiative, is redefining how products are conceived, built, and marketed.

Manufacturers will need to disclose information on product durability, repairability, recyclability, and material composition, enabling regulators, recyclers, and consumers to make informed choices. Similar frameworks are being explored in Japan, South Korea, and India, indicating a global alignment around the principles of transparency and circularity.

The Emerging Focus on Nature and Biodiversity

As the climate agenda evolves, biodiversity and ecosystem protection are fast becoming central to sustainability regulation. The Taskforce on Nature-related Financial Disclosures (TNFD) framework is being integrated into reporting systems, urging companies to measure and disclose their impacts on land, water, and natural capital.

This shift recognizes that climate and nature are interconnected — protecting one without the other is no longer viable.

The New Reality: Compliance as a Strategic Function

Taken together, these frameworks signal a permanent shift: ESG compliance is no longer a reporting function — it’s a strategic one. Businesses that manage sustainability data holistically, anticipate upcoming regulations, and invest in integrated compliance systems will not only avoid penalties but unlock new sources of value — from access to green financing to preferred supplier status in global markets.

In this new era, sustainability leadership will be measured not by ambition, but by auditability.

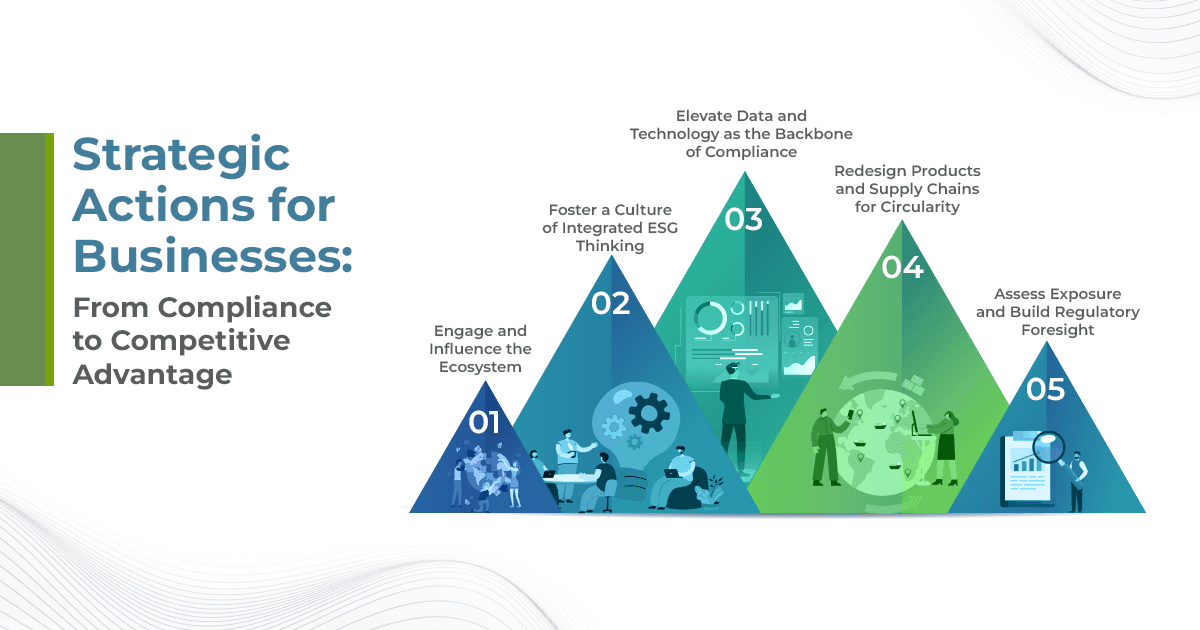

Strategic Actions for Businesses: From Compliance to Competitive Advantage

The next wave of sustainability regulation — spanning EPR, CBAM, CSRD, and beyond — is not merely a compliance exercise. It’s a strategic inflection point that will separate companies that react to regulation from those that lead through it. Businesses that view sustainability as a data and design challenge — rather than a reporting burden — will be the ones to build long-term resilience, efficiency, and trust.

Here’s how forward-looking organizations can position themselves for this new reality:

Assess Exposure and Build Regulatory Foresight: Start with a comprehensive audit of where and how emerging EPR, CBAM, and due diligence laws intersect with your operations and supply chains. Go beyond country-level compliance to understand cross-border overlaps, data dependencies, and future regulatory risks.

Progressive organizations are now building “sustainability regulatory maps” — dynamic dashboards that track which obligations apply to which suppliers, materials, and markets. This visibility turns uncertainty into foresight.

Onlygood’s Take: Through integrated ESG intelligence and supplier data mapping, companies can pre-empt risks and design compliant, future-ready operations — not scramble for data at the last minute.Elevate Data and Technology as the Backbone of Compliance: The complexity of global sustainability regulations demands granular, verifiable, and auditable data. Businesses must invest in systems capable of tracking emissions, waste, product composition, and supplier practices in real time.

AI, automation, and blockchain-based traceability tools are now essential to streamline data collection and reporting, eliminate manual errors, and build trust with auditors and stakeholders.

Onlygood’s Take: Our AI-powered sustainability intelligence platform helps companies centralize Scope 1–3 data, automate GHG accounting, and create audit-ready ESG reports aligned with frameworks like CBAM, CSRD, and EPR.Redesign Products and Supply Chains for Circularity: EPR, ESPR, and circular economy mandates are fundamentally about rethinking design and material flow. Companies that embed recyclability, modularity, and repairability into product design will not only comply — they’ll reduce costs and unlock new revenue streams in secondary markets.

Supplier collaboration is key. Engage upstream and downstream partners to ensure shared accountability for materials, emissions, and end-of-life recovery.

Onlygood’s Take: We help businesses operationalize circularity — integrating lifecycle data and supplier ESG metrics to drive eco-design and waste minimization.Foster a Culture of Integrated ESG Thinking: Regulatory readiness cannot live in silos. True leadership requires embedding sustainability into every function — from procurement to finance to R&D.

Building cross-functional ESG ownership and investing in employee literacy ensures long-term agility and reduces the cost of compliance.

Onlygood’s Take: We partner with organizations to translate ESG policy shifts into actionable internal frameworks — turning compliance from a regulatory cost into a driver of innovation and efficiency.Engage and Influence the Ecosystem: The sustainability regulation landscape is still evolving, and companies that proactively engage with regulators, industry groups, and suppliers will help shape the rules that govern them.

Transparent collaboration, data sharing, and advocacy can help align global standards and reduce compliance friction.

Onlygood’s Take: Through our partnerships with industry consortia and sustainability platforms, we enable our clients to stay ahead of the curve — leveraging collective intelligence to future-proof their ESG strategies.

The Bottom Line

EPR and CBAM are not isolated regulatory hurdles; they represent the beginning of a new era of corporate accountability — one that ties profitability, resilience, and reputation to measurable sustainability outcomes.

For mid-size and large enterprises alike, this is the moment to act — not react. Those who invest now in data transparency, circular design, and digital ESG integration will lead the next decade of sustainable growth.